City of Abernathy Pension Plan

The City of Abernathy is a member of Texas Municipal Retirement System (TMRS) a statewide, multiple employer agent plan. In an agent plan, each participating government’s pension is centrally administered and governed by state statutes but the assets and related pension liabilities for each government are accounted for separately and any unfunded liabilities are solely the obligation of that government. Abernathy has chosen from a menu of plan options as authorized by the TMRS statute. Abernathy’s plan provides the following benefit level:

Related Link

- Employee contribution rate: 5% of pay

- Matching ratio (city to employee): 1 to 1

- Years required for vesting: 5

- Service retirement eligibility: Vested age 60 or 20 years and any age

- Updated Service Credits: 100% repeating, transfers

- Cost of Living Adjustments: 30% of CPI, repeating

- Military Service Credit: Not Elected

- Restricted Prior Service Credit: Yes

- Buy Back Option: Not Elected

- Supplemental Death Benefit (Employees): Yes

- Supplemental Death Benefit (Retirees): $7,500

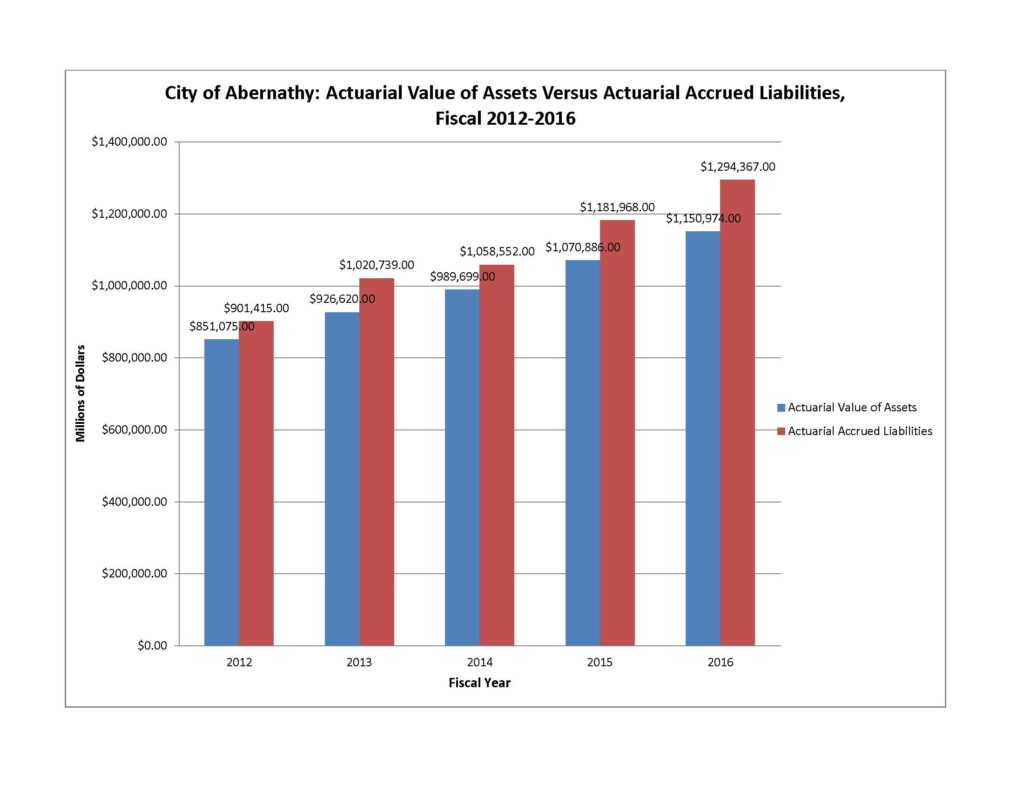

Actuarial Information (as of December 31, 2018)

- Actuarial Accrued Liability (AAL): $1,294,367

- Actuarial Value of Assets (AVA): $1,150,974

- Unfunded Actuarial Accrued Liability (UAAL): $143,393

- Funded Ratio (AVA/AAL): 88.9%

- Equivalent Single Amortization Period: 24.0 Years

- Assumed Rate of Return: 7.00%

- Valuation Payroll: $623,666

- UAAL as a Percent of Covered Payroll: 22.99%

Equivalent Single Amortization Period: The weighted average of all amortization periods used when components of the total unfunded actuarial accrued liability are separately amortized and the average is calculated in accordance with the parameters.

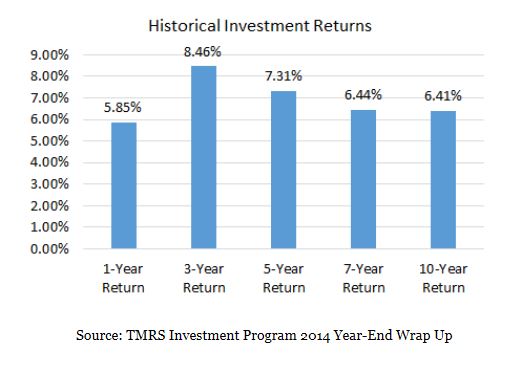

Portfolio Management Strategy

Plan assets are managed on a total return basis with an emphasis on both capital appreciation as well as the production of income, in order to satisfy the short-term and long-term funding needs of TMRS. The long-term expected rate of return on pension plan investments was determined using a building-block method in which best estimate ranges of expected future real rates of return (expected returns, net of pension plan investment expense and inflation) are developed for each major asset class. These ranges are combined to produce the long-term expected rate of return by weighting the expected future real rates of return by the target asset allocation percentage and by adding expected inflation. In determining their best estimate of a recommended investment return assumption under the various alternative asset allocation portfolios, GRS focused on the area between (1) arithmetic mean (aggressive) without an adjustment for time (conservative) and (2) the geometric mean (conservative) with an adjustment for time (aggressive). At its meeting on July 30, 2015, the TMRS Board approved a new portfolio target allocation. The target allocation and best estimates of real rates of return for each major asset class are summarized in the following table:

| Asset Class | Target % | Long-Term Expected Real Rate of Return (Arithmetic) |

|---|---|---|

| U.S. Equities | 17.5% | 4.55% |

| International Equities | 17.5% | 6.10% |

| Core Fixed Income | 10.0% | 1.00% |

| Non-Core Fixed Income | 20.0% | 3.65% |

| Real Estate | 10.0% | 4.03% |

| Real Return | 10.0% | 5.00% |

| Absolute Return | 10.0% | 4.00% |

| Private Equity | 5.0% | 8.00% |

| Cash Equivalents | 0.0% | 0.00% |

Historical Investment Returns

Contributions

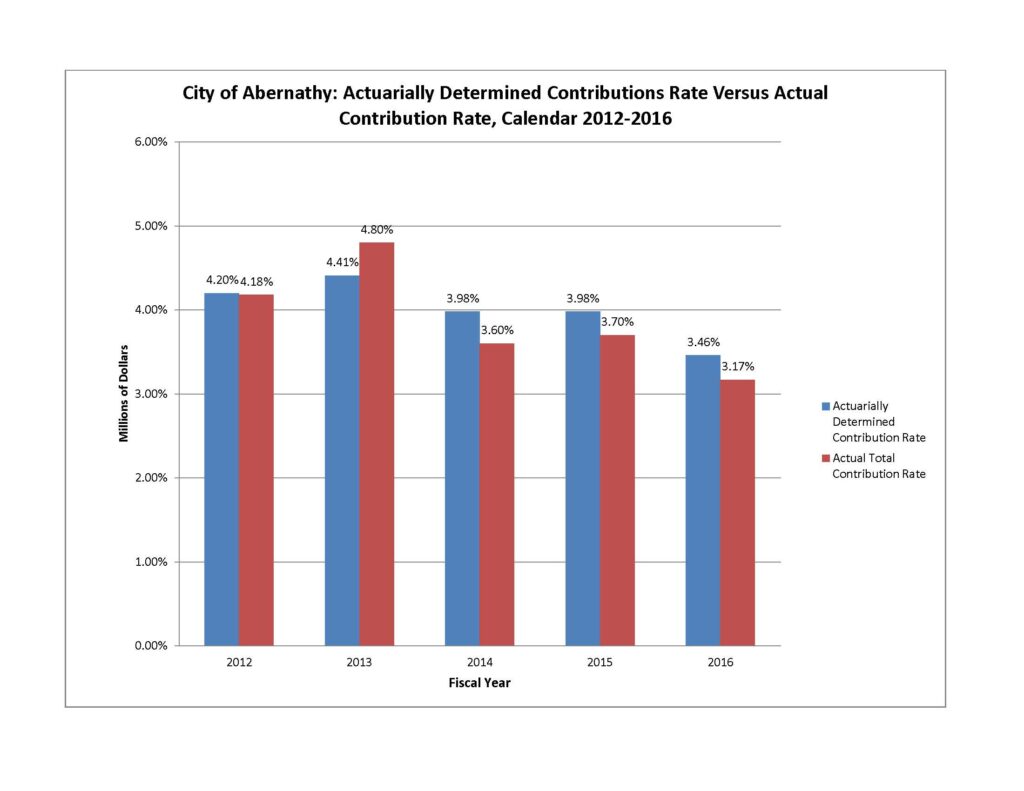

Actuarially Determined Contribution (ADC) rate: A target or recommended contribution to a defined benefit pension plan for the reporting period, determined in conformity with Actuarial Standards of Practice based on the most recent measurement available when the contribution for the reporting period was adopted.

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | |

|---|---|---|---|---|---|---|---|---|

| Employee | 5% | 5% | 5% | 5% | 5% | 5% | 5% | 5% |

| Employer | 4.10% | 3.98% | 3.46% | 3.54% | 4.22% | 4.30% | 4.12% | 3.90% |

| Total Required Contributions | 9.10% | 8.98% | 8.46% | 8.54% | 9.22% | 9.30% | 9.12% | 8.90% |